The metaverse is one of the most discussed digital concepts of recent years – somewhere between visionary platform and overambitious hype. As an immersive, three-dimensional environment in which users interact via avatars, it promises new forms of collaboration and communication – as well as new approaches for the financial sector.

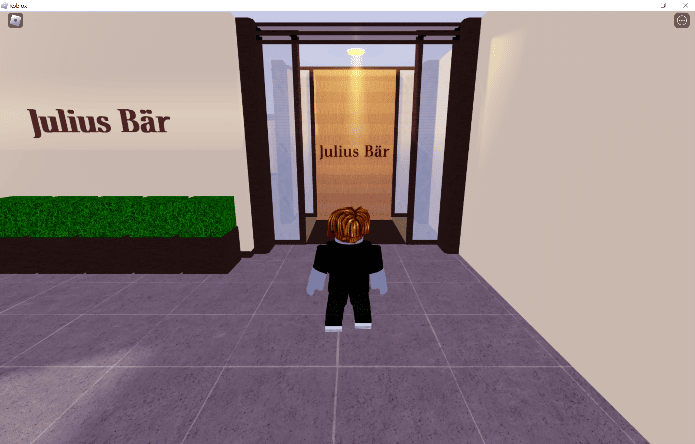

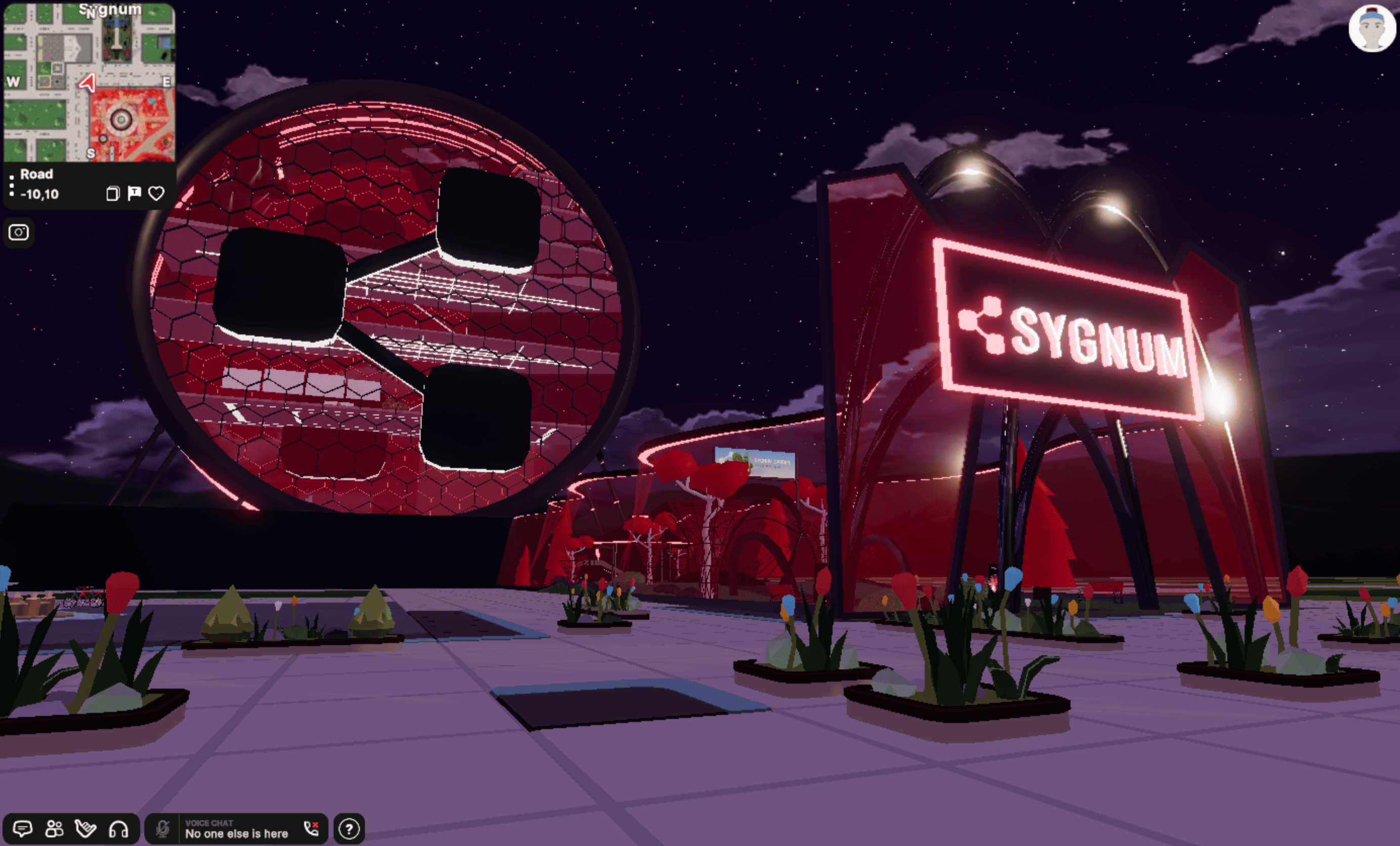

Some banks have already gained initial experience. The Swiss digital bank Sygnum and VP Bank have launched their own implementations in the metaverse. For example, customers can acquire shares in works of art in the form of Art Security Tokens (AST). Julius Bär is also utilising virtual worlds – with the ‘Bär Challenge’, a gamified employer branding initiative to attract young talent.

The Vision: The Virtual Bank Counter

A frequently mentioned application scenario is the virtual bank counter – a fully digital branch in the metaverse. Customers would be able to carry out everyday banking transactions there, from opening an account to consultations and loan enquiries. The first pilot projects already exist in public administration, for example: the canton of Zug also offers selected public services in the metaverse.

Such a digital bank counter could combine traditional services with new functionalities. These include AI-supported advice for simple matters, interactive tools for self-service financial planning, immersive 3D visualisations of complex investment topics and secure transactions based on blockchain technology.

But how realistic is the Virtual Bank Counter?

A survey of selected industry contacts reveals a mixed picture. Although 3D visualisations and avatars are generally viewed positively, the complete relocation of banking processes to the metaverse is met with scepticism.

The main reasons cited are:

- lack of technical expertise for implementation

- lack of trust in metaverse platforms

- unanswered questions regarding data protection and identity verification

- reluctant customer acceptance, especially for sensitive financial topics

Technological hurdles such as device availability or investment costs, on the other hand, play a subordinate role – VR glasses have long since arrived on the consumer market and corresponding platforms exist.

Conclusion: Dreams of the Future with Potential

The fully virtual bank counter remains – as things stand today – an ambitious vision. Although the technological foundations are in place, a lack of trust, legal uncertainties and customer reluctance are holding back widespread implementation.

Nevertheless, it is clear that the metaverse already offers feasible added value in clearly defined use cases such as the visualisation of complex data, virtual events or digital financial education. Formats such as the Julius Bär Challenge prove that younger target groups in particular are open to immersive experiences.

The metaverse should therefore not be seen as a replacement for traditional channels, but as a supplement – where it makes sense and provides real benefits. The future does not lie in ‘either/or’, but in the interplay between physical presence, digital services and virtual extensions. Those who test early on gain experience – and remain relevant even when the next big buzzword comes along.

{kind=link}

{kind=link}

{kind=link}

Author